PDS Limited - Just another Li & Fung or can it be something different

Came across a very interesting business PDS Limited when recently some big names added the same to their portfolio. On the prima facie the business looked quite similar to the long gone superstar Li and Fung Trading Co Ltd but when we delved deeper we found out some key differences. Sharing this note to understand the business end to end and our comments on the business in light of its recent financial performance.

(Source of Information – Co Annual Reports, FAQ’s on co website , Co Investor PPT , Concall Transcripts)

About PDS Limited

PDS was founded in 1999 by Mr. Pallak Seth, who launched two key companies - Norwest Industries in Hong Kong and Poeticgem in the UK. His vision was to create an asset light business model catering to the apparel sourcing needs of retailers and brands. This was then part of House of Pearl Fashion Limited (now known as Pearl Global Industries Limited) which subsequently got listed in 2007. In 2014, PDS demerged from Pearl Global Industries Limited, with the shareholders getting identical shareholding in both companies which continued to be publicly traded on the Indian stock exchanges. Since the de-merger both the companies have been operating independently from each other.

Today, PDS manages fashion value chain for major brands and retailers globally. It has a vast network with over 60 offices across 22 countries and employs over 10,000 people across the UK and Europe, North America, the Middle East, and Asia. PDS acts as a bridge between retailers/brands and apparel manufacturers, offering additional services like design expertise, quality and compliance control, and supply chain management for their international clients.

In the last 5 years, PDS has grown its revenues at 10% and PAT at 27% CAGR and ended up with a avg ROE (post-tax) of 19% . Key value drivers for the firm going forward are increasing share of value-added business, increasing wallet share and synergies between various group companies.

Revenue Streams of PDS

PDS mainly operates under two reporting segments: a) Sourcing b) Manufacturing.

Sourcing

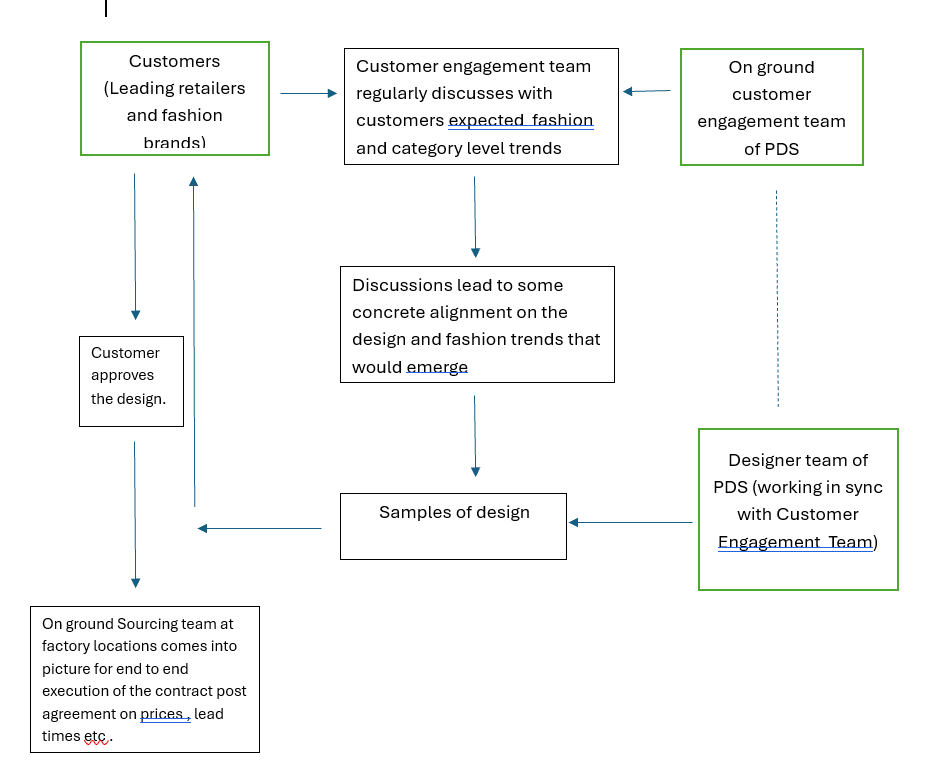

PDS play a crucial role in the fashion industry by facilitating the process of procuring products for leading retailers & brands globally in an asset light way. PDS works with over 600 vendor factory partners spread across Bangladesh, Sri Lanka, Turkey, China, India and others to manufacture apparel and other categories based on the requirements of retailers & brands. As part of its sourcing, PDS manages the entire value chain from market intelligence, trend forecasting, product development, designing, factory identification, pricing & negotiation, order management, quality control amongst others.

Within sourcing PDS has various service offering which includes

Design led Sourcing: In traditional sourcing models, sourcing decisions are often made primarily based on cost, production capabilities, and efficiency. However, in a design led sourcing approach, the design vision and requirements of the product play a central role in the sourcing strategy. With over 250 designers PDS closely collaborates with the merchandising team of retailers and brands for curating customized offerings and then manages the overall sourcing requirements for the same across geographies. As part of this arrangement, the retailer places an order on PDS and PDS in turn places an order on back-to-back terms with a reidentified factory. PDS margins are built in the pricing to the customer.

Sourcing as a service (SAAS) - Essentially managing sourcing offices for retailers/brands in various markets, enabling them to avoid local complexities and relieve management bandwidth of managing large number of factories. Being a cost plus model, the client gets complete visibility & transparency of the costs. This differs from design-led sourcing, which is more seasonal and order-driven. "Sourcing as a Service" goes deeper - PDS essentially acts as the retailer's representative in the market.

Brand Management : PDS has recently moved towards value-added services of brand management. One successful example of the same is the Ted Baker Business. Authentic Brands Group, who owns a large portfolio of successful brands and partners with various players to maximize their value, recently gave PDS a significant opportunity to manage the design and wholesale operations for the Ted Baker brand. PDS now handles a centralized design and sourcing office based out of London. Success in this area could be a major new revenue driver for PDS.

Manufacturing:

PDS had taken a strategic step to enter manufacturing As per them this helps PDS get their foot in the door, since many a time having a manufacturing presence ticks the checklist of the big retailers, specifically in the US. They have manufacturing facilities in Bangladesh (EU/UK tariff-free access) and Sri Lanka, prioritizing ethical labor practices and sustainability. Further, PDS has added specialized plants like centralized cutting plant in Sri Lanka and wash plant in Bangladesh.

Currently the revenue split looks as under

In terms of geographical mix company derives bulk of its revenue from UK (38%) and EU (33%). Almost 13% revenue comes from USA . USA market is still in early stages for the company.

What actually constitutes as revenue for PDS

Under the design led sourcing model and manufacturing business the total volume of business that PDS manages (i.e GMV) gets reported as revenue. However under Sourcing as a Service Model (SAAS) , PDS earns service fees for the volume of the business it manages (i.e. orders are placed by the customer directly on the factory and not only PDS). The reported topline only captures the service fee and not the volume of the business it manages which gets reflected in SAAS.

We have tried to simplify the Design Led Sourcing Business Model which accounts for 88% of revenue and 57 % of EBIT

Further deep dive into the business model of PDS Limited through activities performed under each segment

** We couldn’t find capital employed under each segment seperately in any of the disclosures.

PDS’s unique subsidiary based model (which co claims as its moat )and its rationale (Source – Investor FAQ’s released by the company in May 2024)

One of the key MOAT’s that PDS has is its unique operating model that has evolved over last two decades. This model has its roots in an entrepreneur driven set up. PDS operates +50 verticals and sub-verticals which are led by a business head. This business head and his teamare responsible for managing customer relationship and service deliverability – from getting customer orders to delivering customer orders. Each vertical operates under its ownbusiness head/CEO, fostering a network of established relationships with customers. In order to incentivize industry experts to associate with PDS and become a business head. PDS offers them minority equity stake in their respective businesses. The business head earns a share of bottom-line profit as per his equity stake in turn also making them fully accountable for their verticals entire P&L. They earn this share as a dividend, and this accounted as minority interest in the books of accounts. Business heads have autonomy in running their businesses as long as they operate within the frameworks and guidelines established by PDS and they meet their annual budgets. As a result of this model, PDS operates these many entities since they represent this vertical driven model. An entity driven structure enables PDS to provide complete transparency & autonomy to the business head as they have complete sight of their respective performance. Recently, PDS has been mandated to operate independent entities even by its customers especially for the Sourcing as a Service offering. This enables PDS to provide transparency & visibility to its customers on the costs. PDS empowers leaders to build businesses. PDS supports these businesses by enabling them with working capital limits, HR, IT, accounts, compliance, governance, legal amongst others. Further, PDS is also channelizing collaboration between verticals to cater to a customer or expanding their service offerings

A very good slide from May 2024 PPT to track PDS’s strategic execution going forward

Our observations and concerns post the latest results ( We would be using this as the base for analysing the business going ahead )

Highlights from FY 23-24

- Co GMV for FY was INR 15048 cr vs INR 12059 cr (24.8% YoY growth )

- Gross profit for FY INR 2111 cr vs INR 1771 cr (19% increase in absolute value) (Gross Margin % of 20.4% vis a vis 16.7% in previous year) . Key point to be noted that PDS is not a typical co wherein EV/Sales can be used as a metric as Sales reported is similar to GMV in context of platform businesses. EV / Gross Margin can be the right metric while talking about valuations

- Employee Expenses increased to 979 cr from 761 cr (~ 29% increase). Other expenses 729 cr from 551 cr ( 32% increase). Co said that it has invested in onboarding industry leaders for the growth trajectory ahead. This year was a case of op deleverage . Need to watch how the op leverage plays out in this case in the future . Key point is that in the long run can the company grow its absolute value of gross margins faster than the growth rate in employee expenses and other expenses.

- One time gains on sale of a property which was present last year not there in current year . So considering the fact that employee & other expenses grew at faster rate than the absolute growth in gross margins , there has been a profit decline from 327 cr to 203 cr.

- Cash Flow & Balance Sheet – The company operates on a very thin margin (around 2% of GMV) and hence to generate ROCE , the co needs to be asset light (low capital employed). As a result cash flow and balance sheet needs to be watched cautiously

o Cash flow has capex of 59 cr in 2023 and 167 cr in 2024 respectively. Co in the latest concall said that this capex is mostly in nature of office spaces . Need to cautiously watch the capex trend . Continuous capex is a red flag for the asset light claim

o Working capital days has shot up to 9 days in last 2 years . Co claims excluding the Ted Baker acquisition NWC days is 1 day. Further in the latest call co also claimed that NWC days will be back to early single digits. Need to monitor this going ahead

o Investments in PDS ventures – 70 cr in FY 23 and 29 cr in FY 24 . What is the roadmap for this . Will this be a recurring cash outflow and if yes when would be the respective inflows expected against this

o Cash flow line item – Acquistion of TDG , Nobles and Others – 155 cr outflow in FY 24 and 52 cr outflow in FY 23 . Need to be cautious on this . Co should not go on a spree of acquisitions the Li and Fung way

o Profit sharing with business heads (cash flow line item) – 91 crores in 2024 vs 67 cr in 2023 and Minority Interest in P&L 58 cr in 2024 and 62 cr in 2023 . What is the reason of difference in this . Need to ask the management. Also this is a line item which needs to be watched . The key question is company is targeting in a PAT of 1000 crores in the near term . How much of that will actually accrue to the shareholders after paying for minority interest

Valuations

- Co has guided for a PAT growth of 15% in next FY 2025 with GMV growth of 20% which means there may be another year of op deleverage at play. (though company talks about extracting revenue and profit from investments made in preceding year)

- PAT growth of 15% means 1 yr forward PE of around 36x (assuming 20% growth on PAT available to shareholders in 2024 of 144 cr). On a dividend yield basis the company is trading at a Dividend Yield of ~ 1.15%

- Hence right now we can just have PDS on wait and watch mode . The concerns flagged above needs to be monitored cautiously.

- We have taken a small tracking position . Also valuations look quite expensive considering the current scenario.

Our thoughts :-

PDS prima facie looks a good business with the management till now ensuring that subsidiary based org structuring and design led sourcing creating some differentiation vis a vis the Li and Fung business model. Further company has been very open to engage with investors of late , addressing all their queries . On 11 th June PDS management is also holding an investor day wherein it plans to give investors an opportunity to interact with its top management. The execution has been good despite the poor macroeconomic scenario in last FY. The overall team looks superb with industry veterans and experts.

Our concern right now lies with –1) Whether the co will actually be able to maintain its asset light model and not go overboard with investments in manufacturing and acquisitions - Its very critical as margins of the business are very low and to generate good ROCE its necessary balance sheet remains asset light 2) How quickly will co be able to replicate its success in Europe in other regions especially North America 3) What will ultimately happen to investments in PDS Ventures – what value they will create in the future 4) How much of PAT will ultimately flow to the ultimate shareholders of PDS.

Also as seen in our analysis , Brand Management wherein PDS is taking care of entire value chain from Merchandise Planning to Brand marketing - EBIT margins as % of GMV are the highest. Now the question lies how much incremental capital deployment does this segment actually require vis a vis the incremental margins this segment can generate . May be if management can throw details on this ( Question for the next concall)

Further the valuations also look on the higher side right now . 1 yr forward PE of close to 36x looks expensive for a small cap name and the Margin of safety looks less now given the concerns raised above. We will look forward to get the answers to these questions listed from the management in the coming quarters and valuations to cool down before taking further position in the stock .

Top-notch analysis! Keep up the great work! :-)